Backtesting is a critical process for evaluating the effectiveness of a trading strategy by applying it to historical market data. It involves simulating trades as if they were executed in real-time based on predefined conditions, allowing traders to measure the strategy’s potential performance. This article delves into the mechanics of backtesting, its benefits and limitations, and provides a practical guide to implementing it in the crypto market.

Table Content:

- The Growing Importance of Backtesting in the Crypto Market

- How Backtesting Works

- Historical Data: The Foundation of Backtesting

- Defining Your Trading Strategy

- Incorporating Trading Fees and Slippage

- Analyzing Strategy Performance

- Implementing Backtesting in the Crypto Market

- Utilizing Backtesting Software

- Strategy Selection and Data Collection

- Executing the Backtest

- Analyzing Results and Optimization

- Benefits of Backtesting

- Limitations of Backtesting

alt text: Illustration of backtesting concept

alt text: Illustration of backtesting concept

The Growing Importance of Backtesting in the Crypto Market

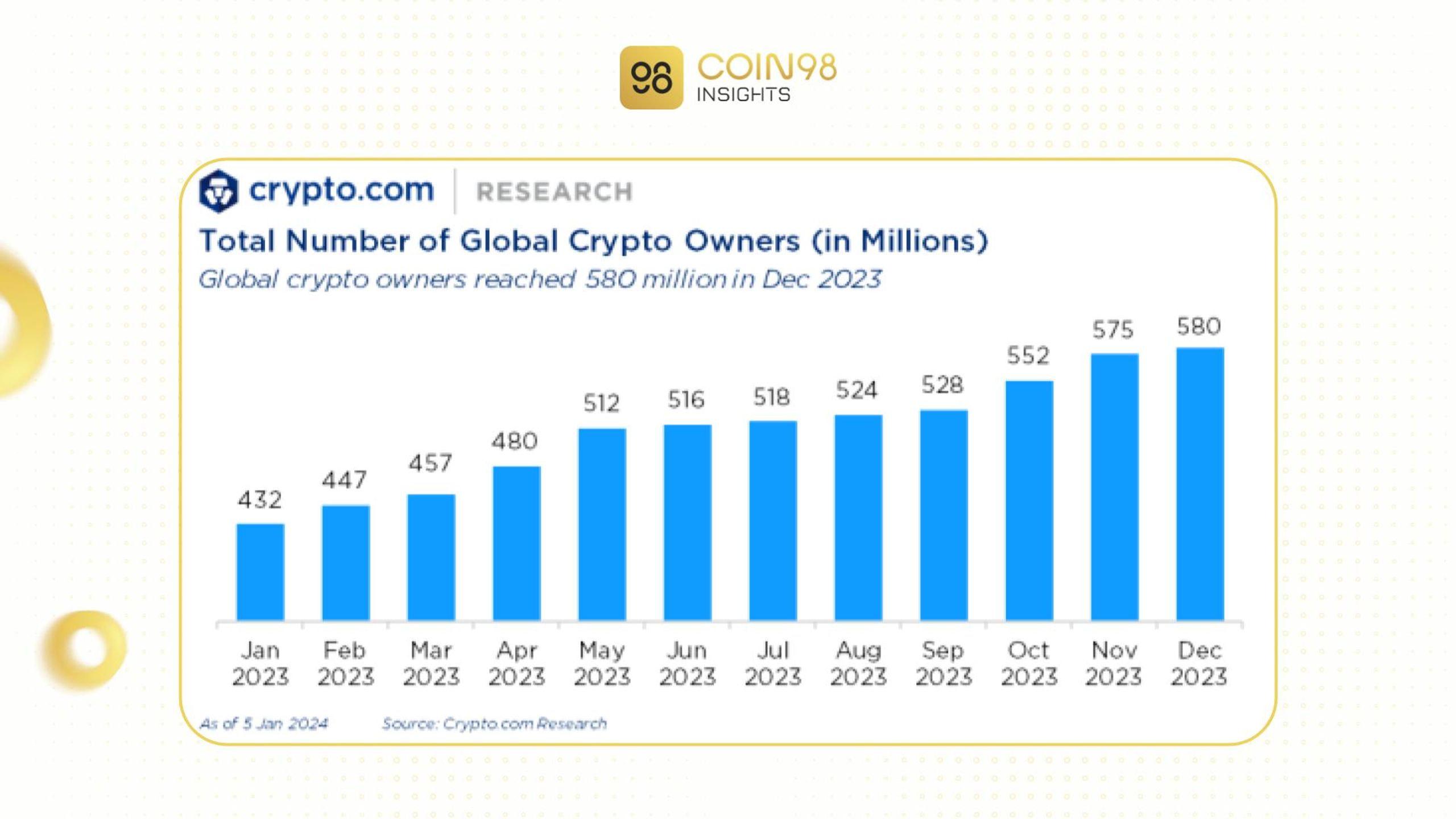

The crypto market’s exponential growth in users and market capitalization, exceeding 580 million global users by the end of 2023 according to Crypto.com, has fueled the demand for robust trading tools. Backtesting allows investors to rigorously test their strategies before deploying capital in the live market, mitigating potential losses.

A 2023 Binance report highlighted the significant role of backtesting in enhancing the efficiency of automated trading strategies, particularly for futures contracts and derivatives. The crypto market’s 24/7 operation and decentralized nature contribute to its volatility and unpredictable patterns, making backtesting indispensable for risk management and strategy validation.

alt text: Graph depicting the growth of crypto users globally

alt text: Graph depicting the growth of crypto users globally

How Backtesting Works

Backtesting utilizes historical data to simulate a specific trading strategy. Traders define their strategy’s rules, including buy/sell signals, technical indicators, stop-loss, and take-profit levels. The strategy is then applied to historical price data, mimicking real-time trading conditions.

For instance, a Bitcoin trading strategy based on the Relative Strength Index (RSI) might involve buying when the RSI falls below 30 (oversold) and selling when it rises above 70 (overbought). The backtesting system would record all simulated trades and calculate the strategy’s overall performance. Key components to consider in backtesting include:

Historical Data: The Foundation of Backtesting

Comprehensive and accurate historical data, encompassing past prices, trading volumes, and relevant market events, is crucial for reliable backtesting results. A larger dataset spanning several years enhances the robustness of the testing process.

Defining Your Trading Strategy

A well-defined trading strategy with clear rules and logic is essential. This includes entry/exit points, stop-loss and take-profit levels, trading volume, and leverage ratios. Strategies can be based on technical analysis (using indicators like RSI, MACD, Bollinger Bands) or fundamental analysis (incorporating news, market events, and policy changes).

Incorporating Trading Fees and Slippage

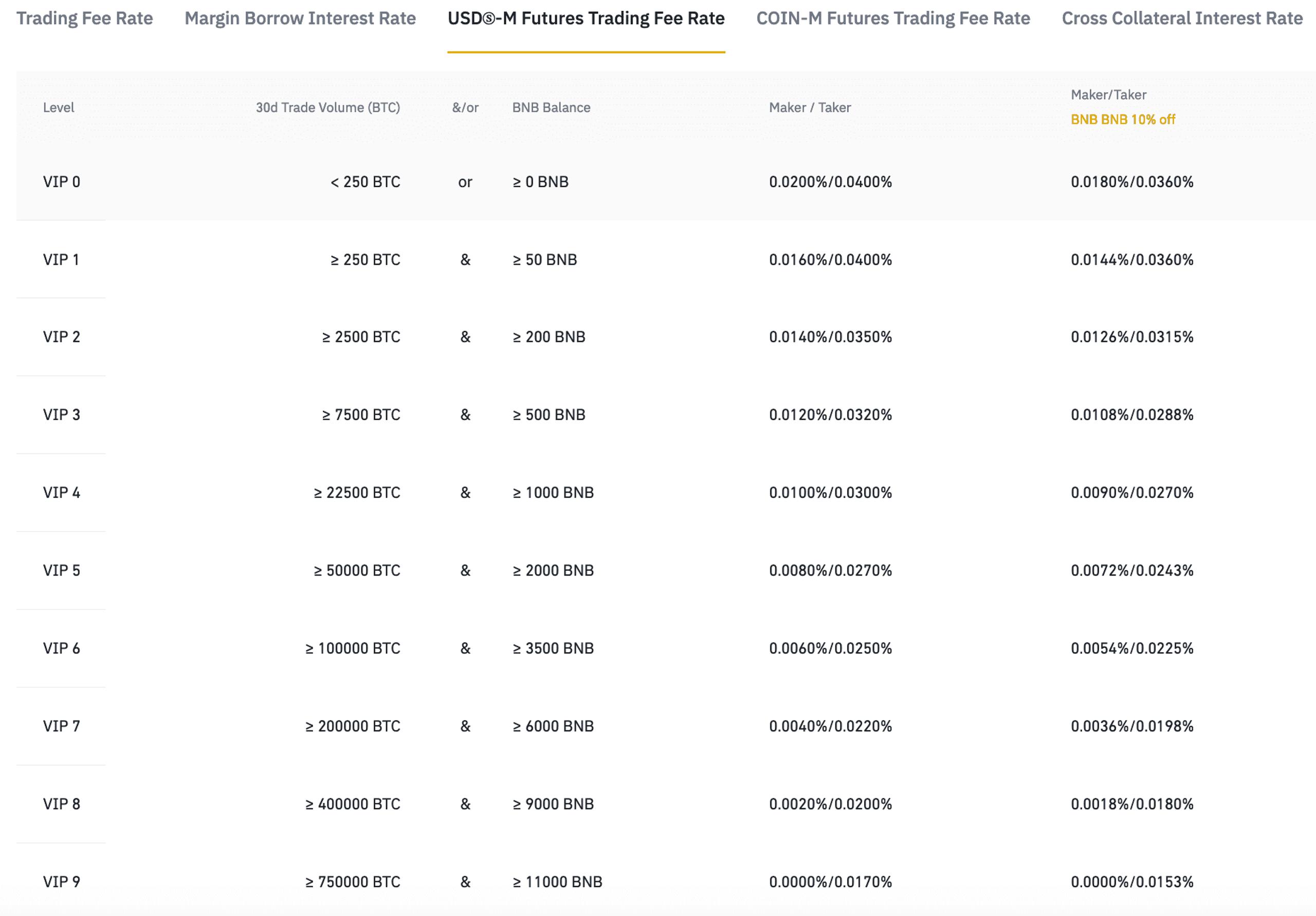

Often overlooked, trading fees and slippage significantly impact a strategy’s profitability. Backtesting should account for fees associated with each trade and potential slippage, especially for low-liquidity assets. These fees can include funding fees for perpetual futures contracts, taker fees for immediate order execution, and maker fees for providing liquidity.

alt text: Table showing different trading fee levels on Binance

alt text: Table showing different trading fee levels on Binance

Analyzing Strategy Performance

Key performance metrics, including profitability, win rate, profit/loss ratio, and maximum drawdown (the largest peak-to-trough decline), provide insights into the strategy’s effectiveness.

Implementing Backtesting in the Crypto Market

Utilizing Backtesting Software

Several platforms facilitate crypto backtesting, including TradingView, Binance Futures, and 3Commas. This guide focuses on backtesting with Binance Futures.

Strategy Selection and Data Collection

Define your strategy’s entry and exit points, take-profit and stop-loss levels, and gather historical data (OHLC prices, trading volume, timeframe) from exchanges like Binance or Coinbase, or via APIs like CoinMarketCap or TradingView.

Executing the Backtest

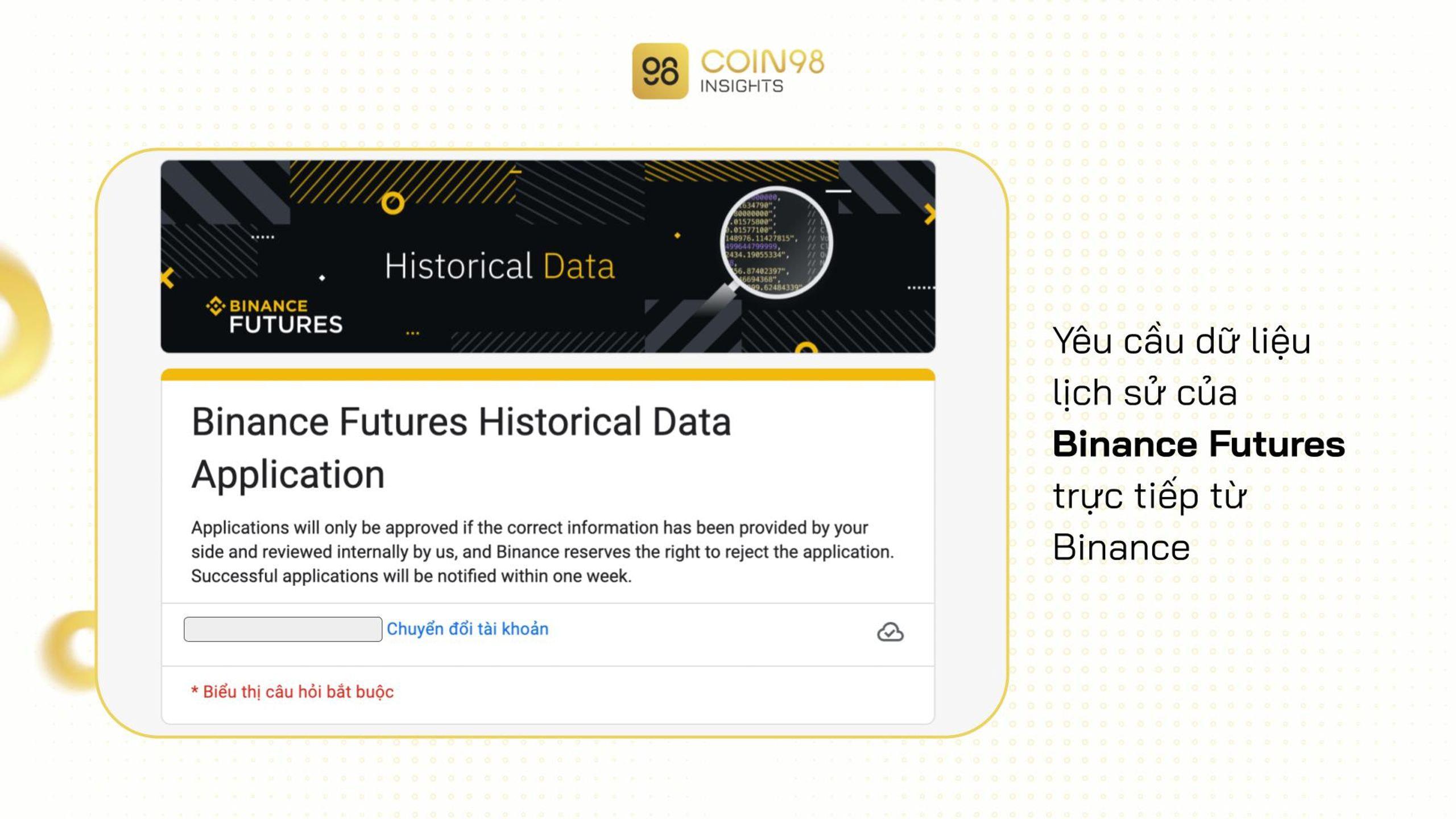

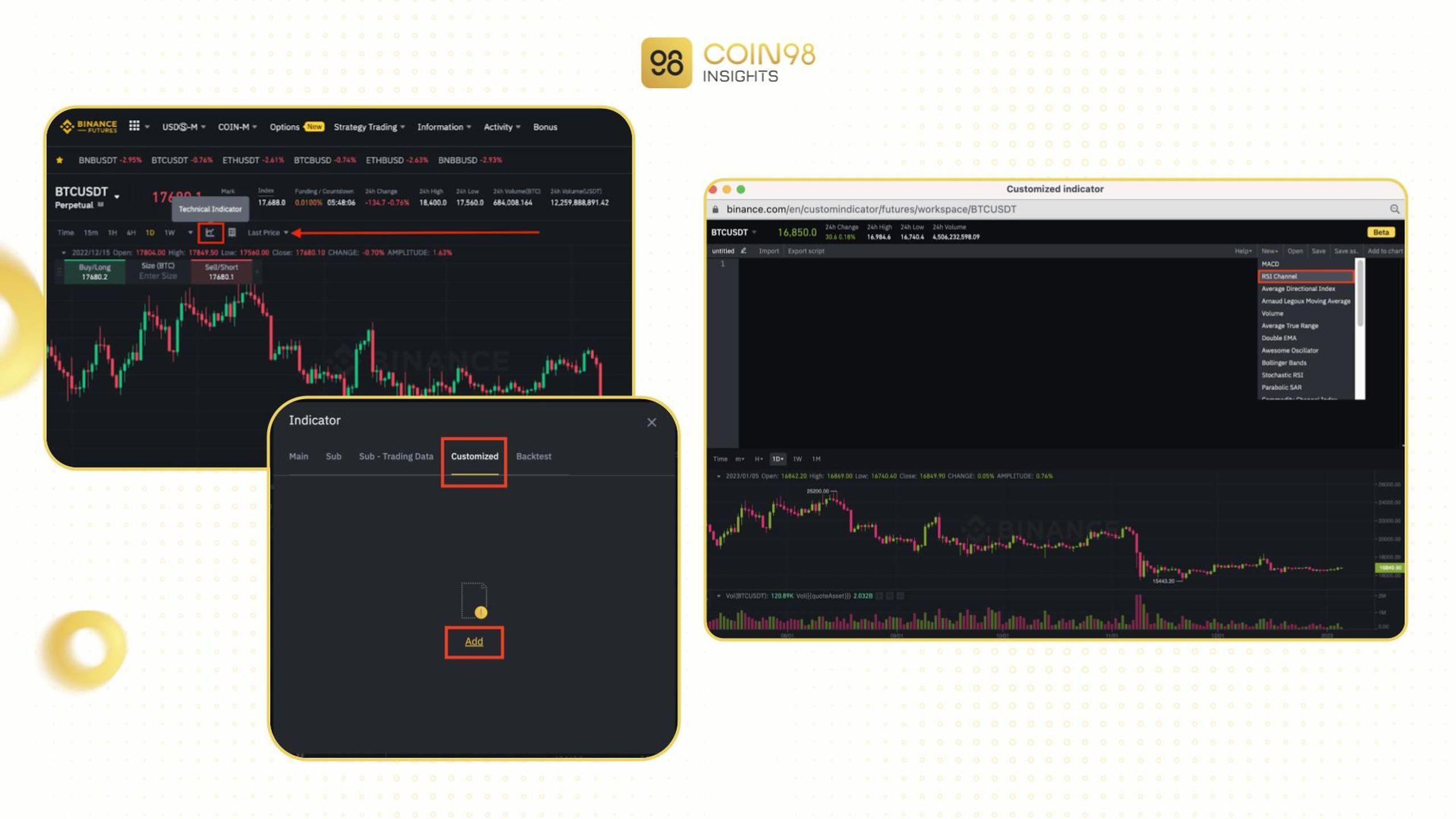

Binance Futures allows direct backtesting. Access the platform, select the trading pair (e.g., BTCUSDT), and navigate to the technical indicators section. Customize indicators like RSI by adjusting parameters and save your settings. Alternatively, manual backtesting involves using APIs to download data and programming the backtest using languages like Python with libraries like Pandas and TA-Lib.

alt text: Screenshot of Binance Futures platform showing data request form

alt text: Screenshot of Binance Futures platform showing data request form

alt text: Screenshot of Binance Futures platform with RSI indicator settings

alt text: Screenshot of Binance Futures platform with RSI indicator settings

Analyzing Results and Optimization

Analyze key metrics like ROI, win rate, and maximum drawdown. Optimize your strategy by adjusting indicators, risk management parameters, and testing different timeframes.

Benefits of Backtesting

Backtesting allows for preemptive strategy evaluation, identification of potential flaws, optimization for improved performance, and builds confidence in trading decisions.

Limitations of Backtesting

Backtesting relies on past data, which may not accurately predict future market behavior. Data inaccuracies, overfitting (optimizing a strategy excessively to historical data), and unforeseen market events can limit its reliability. While backtesting is a valuable tool, it should be used in conjunction with sound judgment and a thorough understanding of market dynamics.